Greetings ladies and gents! I have been meaning to collect my thoughts on the curious case of the BoJ for a few weeks. As a global spectator, the Japanese economic situation stands out. Foreign investors have placed a direct challenge to the BoJ’s yield curve control policy, placing investors and the central bank in direct conflict, resulting in whipsaw trading in the FX markets. This kind of volatility has been difficult to navigate as a trend trader, so I have abstained from serious trading. I believe we now find ourselves in a situation with some foothold, where there is enough information to make a substantive enough picture for trading. The carry-trade is always an enticing opportunity as a trend trader. I find the current USD/JPY set up sufficient enough for consideration in the medium term.

We will start off with

A Bit of Recent History

-

March-October 22—USD strengthens approximately 25% against JPY as the Fed continues to hike rates. The BoJ holds rates steady, maintaining yield curve control, buying Japanese Government Bonds (JGB’s) en masse.

-

October 22—Traders pour on bets in the FX market as the swap rate between USD and JPY continues to widen. The BoJ says that it will defend the Yen by intervening in the FX market, flooding the market with dollars, and U.S. denominated bond holdings. Traders know that this is not a sustainable policy. The BoJ will have to relent in a substantial way, either by raising interest rates or loosening their grip on JGB yields.

-

End of October-Early November 22—Rumors abound that the Fed is nearing the end of its tightening cycle, stirring up optimism in U.S equity markets. Traders continue to stack bets against the BoJ. The BoJ intervenes above the psychological 150 USD/JPY level, pushing the pair to 146 USD/JPY. For the next few days, traders continue to challenge the 150 USD/JPY level.

-

November 10, 22—The October CPI report is released, showing the first signs that U.S. inflation is beginning to slow, and concretizing the rumors surrounding future Fed rate hikes. The top of the tightening cycle is near. USD/JPY drops 600 pips in a single day. The USD/JPY carry-trade is effectively over, saving the BoJ from further intervention in the FX markets.

-

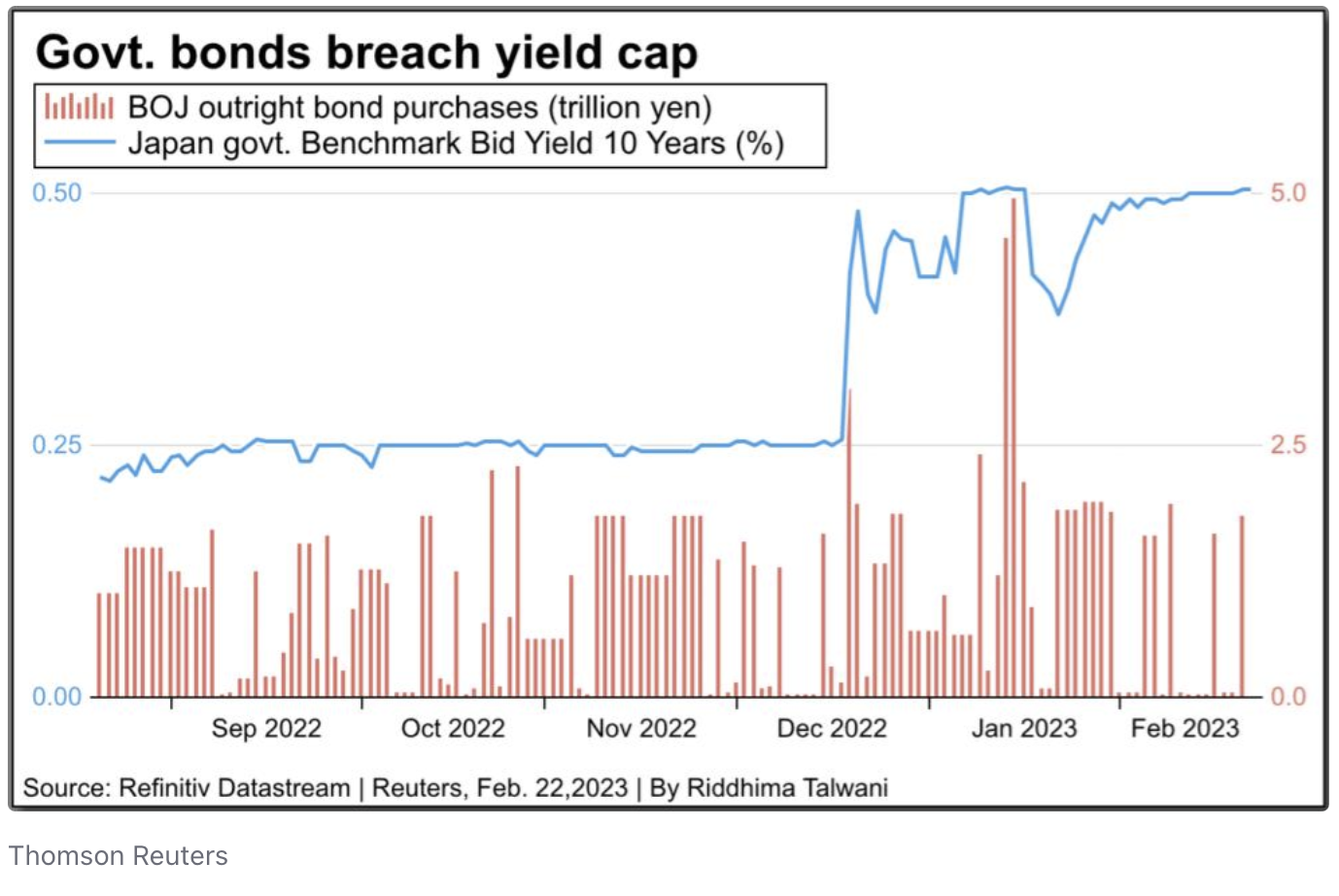

Mid November 22-Mid January 23—USD/JPY comes screaming back to Earth. Falling from 142 to 128 on continued optimism that US inflation is coming down, and US economic data is firmer than expected, a recession might be avoided after all. Speculation over a new BoJ Governor in April contributed to the unwinding, as did a surprise policy shift by the BoJ, where they lifted their yield curve control cap on the 10-year JGB from 0.25% to 0.5%. Further increases could see strong Japanese capital inflows for the first time in decades.

-

February 2, 23—Fed Chairman Powell essentially confirms the US market’s optimistic projections. The Fed will act according to data going forward.

-

February 3, 23—Nonfarm Payrolls are released: total nonfarm payroll employment rose by 517,000 in January, and the unemployment rate changed little at 3.4 percent. These figures are much stronger than expected. The labor market is the strongest it has been in decades, spelling trouble for the Fed, as the last hurdle contributing to high inflation is the wage-sensitive category, Core PCE Services ex-Housing.

-

February 3, 23-Present—A softer CPI reading is not enough to deter investors, economic data remains strong. The overtly optimistic market sentiment, which projected Fed rate cuts by the end of the year, has evaporated overnight. In the weeks following, the market has slowly attuned itself to the Fed’s ‘higher for longer’ projections.

USD/JPY Looking Forward

The path forward for the BoJ is less than ideal. Hard-nosed yield curve control has made the BoJ the last dovish holdout among central banks. The bond market, particularly foreign investors, are shorting JGBs, speculating that the incoming governor Kazuo Ueda will do away with yield curve control altogether. In January, the BoJ purchased more JGBs, and thus added more liquidity to global financial markets, than the Fed, ECB, and the BoE took out of it!1 This is certainly contradicting the effectiveness of the tightening policies by other central banks for the time being.

Since the jobs report released on Feb. 3, FX markets have been dominated by dollar strength. The DXY channel has been slowly but steadily rising, giving one the sense of some resistance by traders to reverse recent course.

Cases for a Stronger Dollar / Weaker Yen

What would qualify the continuance of the ‘higher for longer’ channel?

-

BoJ Governor Kuroda defends yield control up to the end of his term in April;

-

New BoJ Governor Ueda is more dovish than markets anticipate him to be;

-

A lower Japanese inflation reading;

-

Core PCE Services ex-Housing remains resistant;

-

Any (CPI, PPI, PCE) inflation index indicating that price increases are settling (and not slowing) above the Fed’s 2% target rate;

-

Discussions of a 50 basis point hike leading up to, or multiple 25 basis point hikes after, the March FOMC meeting.

Cases for Stronger Yen / Weaker Dollar

What would qualify as a meaningful disruption to the ‘higher for longer’ channel?

-

BoJ ends yield curve control;

-

BoJ raises short-term deposit rate above 0;

-

Core PCE Services ex-Housing falls dramatically;

-

January NFP report is revised down, February report nullifies some of the January reports potency;

-

The Fed maintains data-driven language, which comes off dovish.

The Case For Now

For the meantime, the carry-trade is back on. USD/JPY is testing 135. We have witnessed an aggressive move up, and if nothing changes, this will likely continue into March. I see a retest of the 138 level as a possibility, 140 if US data continues to be strong. On the other hand, the cases for a stronger yen/weaker dollar present the opportunity for a dramatic slide. To trade under these conditions, I will be placing bets with tight stops, which will be tricky because I want to capitalize on the carry-trade while minimizing my risk of loss against a slide. And if the slide does come, I will look to participate in it. There are a lot of events to pay close attention to in the coming month for the USD/JPY pair. I will continue to monitor the Fed and BoJ stances, US and Japanese inflation reports, and US jobs reports. Given the amount of recent volatility, there is a lot of opportunity here to profit in either direction with intelligent betting strategies.

Upcoming Events affecting USD/JPY:

-

US PCE Price Index, Core PCE Price Index—2.24

-

JP Inflation—2.24

-

US Durable Goods Orders—2.27

-

US ISM Manufacturing PMI—3.1