Greetings ladies and gents! We are on the brink of closing out the first month of 2023—the year that every analyst and their mother predicted would be a year for hard financial times. Since our last update, we have been watching the EUR/USD pair closely. In our last analysis, we surmised that the 1.07 level might be the peak resistance level that traders would be unwilling to crack open, after a meteoric rise up from the ashes when the pair was trading at 0.95 last October. As a matter of fact, the days after that prediction was made, the pair cracked 1.07, 1.08, and eventually 1.09 as traders continued to speculate over future Fed and ECB monetary policy. Speculation has been fueled by

-

some lower inflation data from both economies;

-

the inability of US government officials to raise the debt ceiling;

-

the economics of ongoing war in Russia and Ukraine;

-

leading economic indicators like the Manufacturing and Non-Manufacturing PMIs and Retail Sales estimates;

-

as well as a host of other factors.

While we maintain our stance that the dollar is oversold at this late stage in an extreme short rally, this time we come bearing more evidence that the rally, against the Euro, the Yen, and the Canadian dollar, but particularly against the Euro, has reached its peak. Below, the evidence.

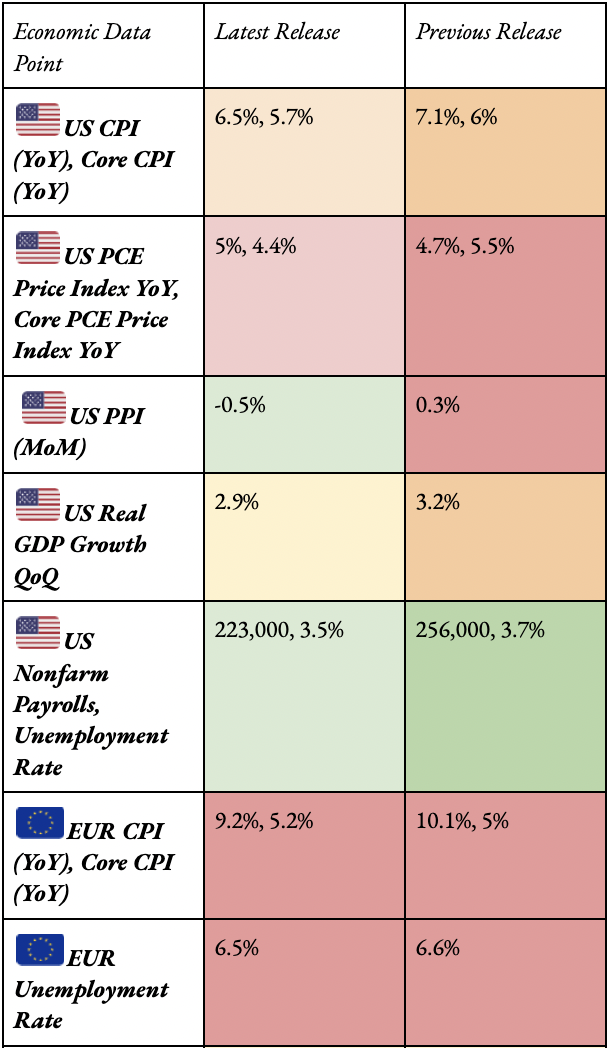

But first, let us examine some of the major data points:

While headline inflation data has been on a downward trajectory, there is a long road ahead before inflation is at or below central bank target rates of 2%. The Fed faces a strong labor market, where demand is sufficient that workers can demand higher wages to compensate for higher costs they face as consumers. The ECB faces high energy prices that have spread into food and service costs, making the issue increasingly more complex. For both economies, the imminent reopening of China will instigate increased global demand, meaning prices will remain higher for longer, especially in energy markets, which have plagued Europe for some time. It is possible, if not likely, that inflation rates begin to level out in the 3-5% YoY range. With 2% inflation targets, will the Fed and ECB relent to the markets, or will they continue tightening (QT) until the job is done? Regardless of outcome, the era of free money is now behind us.

So why do we propose the euro is overvalued against the dollar?

To answer this, we must first outline the reasoning behind the meteoric reversal in fates that drove the EUR/USD pair, first on a steady decline down from 1.10 to 0.95, then rising in a near perfect reflection up from the 0.95 low in October to the 1.09 level today.

In the run down to 0.95, markets were processing unknowns—the strength of inflation, and following, just how hawkish the Fed would need to be in order to tame it. When the Fed turned aggressive, raising interest rates by 75 basis points at 3 consecutive FOMC meetings, the rate ceiling was uncertain, and thus could not be properly priced. The demand for dollars increased, however, as the interest rate differential between the US and Europe continued to widen with each meeting. Eventually, the ECB followed suit by raising their deposit rate, but faced with a different set of economic conditions, they did so less aggressively.

The October CPI report was the inflection point that began the unwinding of the long dollar trade that spanned the better part of 2 years. The report showed the first evidence that the inflation rate had peaked, and traders felt confident enough that they had a bound with which they could sufficiently price real future interest rates. Suddenly, the peak Federal Funds Rate that could have gone as high as 7% was now expected to peak between 5-5.5%. Longer duration treasury yields slipped below short duration yields, as the bond market expected inflation to dissipate within the year. Foreign demand for treasuries evaporated, as hopes of competitive domestic yields increased.

From a logical standpoint, the unwinding of the long dollar trade makes complete sense. The uncertainty surrounding the Federal Funds Rate had come to an end, and the market found it had overpriced its expectation of yields. What is troubling is the reaction to the new confidence bound around 5% yields. In the months following the October CPI report, the FX markets became increasingly volatile. The yen, which had weakened all the way from 110¥ to 150¥/$ over the prior 9 months of 2022, collapsed to 130¥/$, a seismic 13% shift—far higher than any bond trader would expect to yield by shifting their bond portfolio to domestic holdings. Perhaps traders were capitalizing on the exchange rate move as their expected return on investment in the US declined. Throughout the hiking cycle up to that point, high yielding treasuries accelerated foreign demand for the dollar on a consistent enough incline that interest rate + currency appreciation made for a particularly handsome return. Once the peak interest rate was more or less known however, foreign demand evaporated, and even reversed, as traders sought to realize the currency appreciation they had gained since entering the trade. Similarly to the yen, the euro, which, prior to any central bank interest rate hikes, was trading at €1.10, had steadily declined to €0.95/$, and in the months following October, has retraced almost completely to €1.09/$.

4 months after the fact, central banks have followed the expectations they set forth with forward guidance to the letter, as we expect the Fed will continue into the release of tomorrow’s interest rate decision. The markets have had sufficient time to adjust, and yet the EUR/USD exchange rate is trading near its 2 year high prior to any interest rate hikes. Now, the economies are in materially different places: most would say the US is the odds on favorite of the two economies in terms of 2023 performance, and interest rates in the US are 225 basis points higher than their European counterparts.

The Case for a Reversion

We want to make the case that the most recent appreciation of the euro against the dollar is once again, an example of trader’s abuse of speculation.

-

While the ECB deposit rate will likely increase, expectations of the terminal rate rest currently at 3.25%, lower than the current federal funds rate of 4.5%, which will be increased on Feb. 1 and likely again at the March FOMC meeting.

-

While interest rates will converge, it is unlikely that they converge to the differential prior to interest rate hikes (where EUR/USD was trading at 1.10). We believe traders should expect a differential of 150 basis points favoring the US over Europe in the medium-term future.

-

While clear currency appreciation is no longer an attractive aspect of the long US treasury trade, higher yields will, once again, attract foreign demand.

-

The short dollar trade is overcrowded. The Fed would like to take money out of circulation. If markets continue to rise on unfounded optimism that inflation is in full retreat and the Fed will begin easing by EoY, paradoxically, the Fed will have to maintain hawkish policy for longer until the market begins to behave rationally. An increasingly large role of the Fed is to keep market expectations in line.

-

The EUR/USD pair has shown a significant loss of momentum above 1.09, and has since retreated as low as 1.08.

For these reasons, I expect that EUR/USD will revert toward the center of the move from 0.95 to 1.09. Let us assume that traders had priced in a 7% federal funds rate and a 4% deposit rate at the ECB. This 300 basis point differential has now been cut to 150 basis points. The currency pair ought to have settled around 1.02-1.04. Instead, it has traversed back to 1.09. That discrepancy, we believe, will be corrected in the coming months, particularly as markets discover that central banks intend to follow forward guidance despite volatility caused in financial markets.

Tomorrow, the Fed will raise interest rates by 25 basis points. The market believes this is a near certainty. On Thursday, the ECB will raise interest rates by 50 basis points, closing the interest rate gap to 1.75%.

As always, we advise that you do not predict the market, but rather react to the opportunities the market gives you. This entire analysis is a set up for an opportunity, not an opportunity itself. For now, we wait for the short dollar trade to show us its last gasps of upward momentum. The return of the dollar will be a highly profitable opportunity, not as profitable as its unwinding, but at least as profitable in terms of risk/reward, and it aligns with current interest rate swaps.

Do uncertainties remain? Of course. We do not know which central bank will decide to ease first. But we do know the timeframe for this is beyond the predictable future. We do not know how the reopening of China will affect the prices of commodities, or how directly shifts of supply and demand upon its re-entry will affect inflation in the West.

We believe the speculative EUR/USD bias remains slightly bullish, but due to the overcrowded nature of the trade, there is far more downside potential than upside at this late development. Markets in the US are acting in defiance against the Federal Reserve. Given the risk-free opportunities for yield available, this display is an act of outright irrational exuberance. The demand for the dollar should return as the supply of dollars decreases (through Quantitative Tightening money will evaporate from the Fed’s balance sheet). We believe the Fed will do as it says, meaning that while rates may not eclipse 5-5.25%, they will be held at this rate until inflation is sufficiently tamped out of the system, as evidenced by lower CPI, PPI, and PCE readings, but especially by evidence of decreased wage growth. The market seems to discount the possibility that inflation, while on the decline, will continue to be volatile. The opportunity cost of defying the Fed is very high when the risk-free alternative is a 5% return. We believe that the time for the dollar to retrace some of its late losses is on the horizon. For now, we wait for price action to affirm the move.

Upcoming events affecting EUR/USD:

-

US Federal Reserve Interest Rate Decision—2.1

-

US ISM Manufacturing PMI—2.1

-

ECB Interest Rate Decision—2.2

-

US Nonfarm Payrolls—2.3

-

US ISM Non-Manufacturing PMI—2.3