Greetings ladies and gents. Wishing you and yours a happy and smooth transition into the new year! In December, the anticipation of how the U.S. economy would shake out in 2023 consumed our attention. Now, the time is (sort of) upon us. FX volatility, which was historically high throughout 2022, will remain high as long as central bank policy diverges. Q1 ‘23 will be telling as:

-

the employment situation in the US;

-

continued energy supply concerns in Europe;

-

and recession probabilities

continue to shape the Fed’s and the ECB’s policy stances. For the time being, we continue to heavily monitor the indicators regarding inflation, the strength of labor markets, and the price of oil and other energy products. We believe shifts in these indicators are dictating the supply and demand for euro and dollars, as traders and investors are behaving out of short-term speculation, but hesitant to make any long term decisions until markets are sufficiently certain of direction. We will take all of this into account as we take on positions in the coming month.

Recent inflation measures in Europe sparked a downturn in the currency pair for the first time since November.

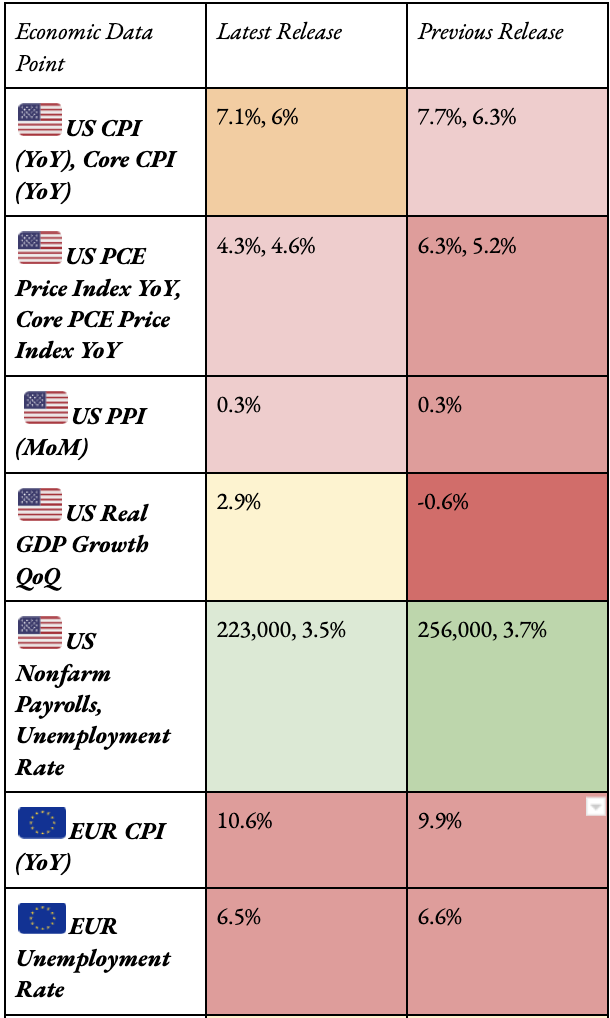

On Friday, we witnessed a strong employment situation report out of the U.S—nonfarm payrolls came in stronger than expected at 223k (200k expected), and the unemployment rate dropped from 3.7% to 3.5%. From the Fed’s viewpoint, the labor market remains very strong which it sees as an obstacle toward lowering inflation. The strong labor trend increased the probability of hawkish Fed policy, and yields rose slightly, giving the dollar a boost.

However, soon after the Employment Situation was released, the ISM non-manufacturing PMI report handed the market a different, and seemingly contradictory, narrative to consider. The index fell sharply from 56.5 in November to 49.6 in December. PMI indexes are centered around the number 50, with readings less than 50 indicating a decline in business activity, and readings greater than 50 indicating an expansion of business activity. The 49.6 reading was far below expectations of 55. The non-manufacturing PMI index reports changes from month to month in business activity, orders, deliveries, and inventory. A slow-down in these areas is a nod acknowledging higher interest rates are beginning to have their effect on the economy. Investors reacted sensitively to this reading, as the natural effect of a decline in business activity is a weakening labor market. The 10-year treasury note yield fell by 4.3% on the day. Stock market indexes, somewhat paradoxically, rallied on the likelihood of the called for recession increasing. USD demand dropped sharply, resuming its medium-term bearish trend.

The battles against inflation in the U.S. and Europe are characteristically different.

In Europe, the ECB faces supply-driven inflation which can be greatly attributed to the conflict between Russia and Ukraine. Russia has been a supplier of natural gas and oil to the European continent, and due to sanctions, these supply lines have had to be re-routed, increasing the cost of energy significantly. The ECB faces soaring inflation and serious concerns that inflation could become entrenched in the labor market, but there is little a central bank can do in the effort to address supply-driven inflation. Additionally, the labor market in Europe is fragile, and the risk of recession is high. Of course, a resolution with Russia could have a very immediate and volatile effect on the Euro.

In the U.S, the Fed faces demand-driven inflation sparked by its own massive pandemic stimulus efforts throughout 2020. By significantly increasing its asset purchases with new dollars, the economy boomed with low borrowing rates. Asset prices rose dramatically from their 2020 March lows throughout 2021. In 2022, these gains sparked inflation, which began as “transitory” supply-chain slowdowns and quickly spread into food and energy prices. To compensate, wages in the labor market have increased, further entrenching price increases. Meanwhile, asset prices have fallen, interest rates are at their highest in over a decade, and the cost of new debt is beginning to be felt by the American public. The Fed’s view is that in order to hedge inflation risk, it must see significant decline in wage growth to ensure that high inflation is sufficiently tampered out of the system. The path toward lowering demand-driven inflation is straightforward; nonetheless, it will be a painful one for the U.S. economy as the risk of a recession in 2023 is significant.

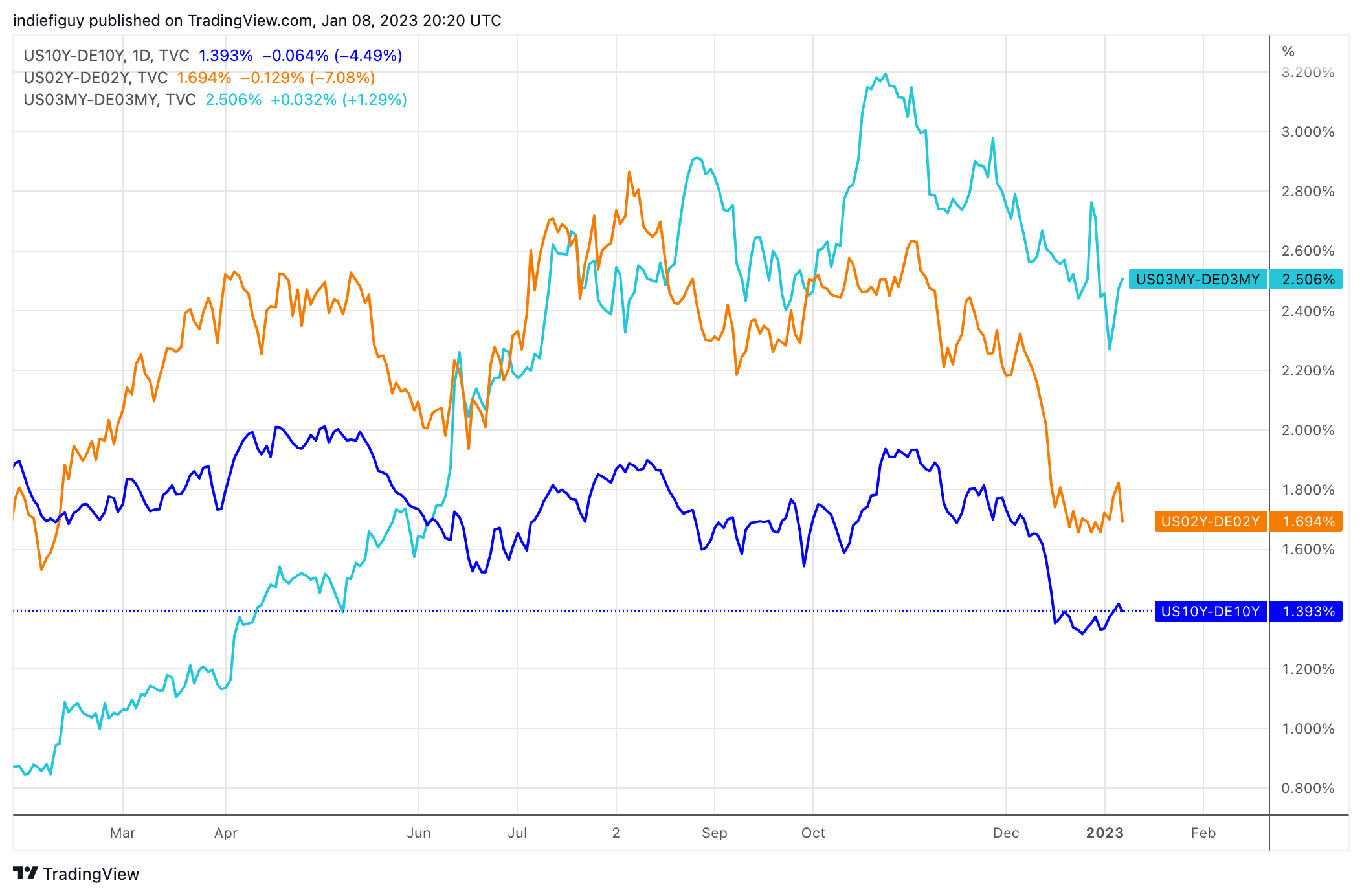

We believe that the primary demand driver in regards to the EUR/USD pair is interest rate differential. Hence, speculation toward the direction of future interest rate policy, and its effect on bond yields is driving the exchange rate as we await concrete economic data and subsequent central bank policy changes.

The interest rate differential between U.S. and German bonds has been steadily decreasing since the middle of October 2022. While the yield differential is currently in favor of U.S. rates, speculators expect the differential to decrease as rates are close to peaking in the U.S. and European rates maintain some upward potential. Even so, it would seem that 1.07 remains a strong consensus price with regard to future rate convergence. Volatility for EUR/USD will remain until central bank policy is more certain. We continue to watch for events that may shift the narrative in favor of one side—oil and natural gas prices, bond yields, inflation reports, business manufacturing and production, the Russia-Ukraine conflict. News regarding these topics will continue to supply exchange markets with volatility as investors determine whether to invest domestically or abroad.

For now, a few questions remain to be answered: Which central bank is more likely to cut rates first? Will the U.S. slip into a recession? Will Europe? If so, will the recession be light or severe? Will the conflict between Russia and Ukraine resolve itself peacefully—in favor of the Western powers? Where has demand for U.S. treasuries gone when yields are at their highest since 2008? Is the mass exodus from treasuries a rational one? Will demand return with higher commodity prices?

We believe the speculative EUR/USD bias remains toward the upside, but it is possible that the upside has limited profit potential as the pair has attempted to break above the 1.07 handle a multitude of times on its bull run and has failed to do so with any veracity. The pair has certainly been more willing to float upward, and has exhibited stronger sensitivity to bearish U.S. news than bullish European news. But while the bullish trade appears to be the path of lesser resistance, in our opinion the trade lacks enough reward to justify holding negative interest parity.

Upcoming events affecting EUR/USD:

- U.S. CPI (Dec. Estimate)—1.12