Greetings ladies and gents. Tomorrow’s headline news event is the U.S. PPI report. Does this report have the capacity to move markets? Potentially. The flows out of equities into bonds this week have shown that market participants are being reminded of the disruption that sustained high interest rates could cause throughout 2023. Market participants are fading the optimism surrounding a Fed pivot stance until more data is available. A dramatic cut to the November inflation rate could be a catalyst for renewed optimism. Since oil has fallen significantly since October, it is certainly possible that the PPI rate could fall as described. Alternatively, the PPI figure could come in as expected, or worse, and the equity fade would likely continue into next week’s FOMC interest rate decision. I expect DXY to follow the path of bonds here as the interest rate decision next week comes into full focus. These are the considerations we are considering when putting on positions this week.

The following is my current outlook for USD/CAD, which I believe is poised for further upside.

First, the data points:

We begin by analyzing the state of the U.S. economy, as forecasted by the U.S. treasury market.

The deviation between U.S. short-term (2Y) and medium-term (10Y) yields continues to increase, suggesting that bond traders have pivoted their concern away from peak inflation to the downside risks of global growth. Employment data suggests that the Federal Reserve’s rate hikes have not instigated significant change in the labor market yet, and therefore high inflation rates may not fall as quickly as hoped. The inversion of the yield curve is a strong predictor of a recession. Yields have been inverted since July. If hints of a global recession reveal themselves, and the Federal Reserve holds rates steady, investors will return to the dollar, as U.S. government bonds will become increasingly attractive with their high risk-free rate.

Now, we turn to crude oil—an ongoing quasi-stimulus package to U.S. consumers and businesses alike.

U.S. oil has fallen since its peak in July due to a number of factors. The most important, the looming threat of global recession, has threatened demand for crude oil. In tandem, the U.S. government has been increasing supply in the markets by awarding contracts of oil stocks from the Strategic Petroleum Reserve (SPR) to refineries. The final release contract for sale of SPR crude oil ends Dec 31. Now, the SPR stock has fallen approximately 36% from this time last year, and it sits at approximately 55% of capacity. The U.S. government has stated that it will begin refilling the SPR at $70/barrel. While this rate is not enticing to crude oil extractors, it guarantees demand, creating a price floor at $70/barrel.

Energy has been a large contributor to the unexpected rise in inflation. The war in Ukraine has sparked an energy crisis as Western nations have been politically inclined to sanction Russian exports, including oil and natural gas. While the crisis is more central to Europe, the decrease in sanction-less supply has been felt globally. But since July, supply concerns have cooled, and along with those concerns, the price of oil has fallen.

We turn our focus back to the trade at hand, USD/CAD. Why is the price of oil relevant to this currency pair?

Canada’s largest export goods are crude oil, motor vehicles, and gold. The production and delivery of oil products, natural gas and electricity in Canada contributes about $170 billion to Canada’s $1.8 trillion GDP, or just under 10%. Oil extraction companies are very responsive to changes in the price of oil. They use future projections of the price to allocate investment toward their variable costs of production. Therefore, the price of energy has a significant effect on Canadian GDP. Crude oil and motor vehicles are both demand driven goods. A U.S. recession—the U.S. is Canada’s largest trading partner—could cause a significant slump in Canadian exports.

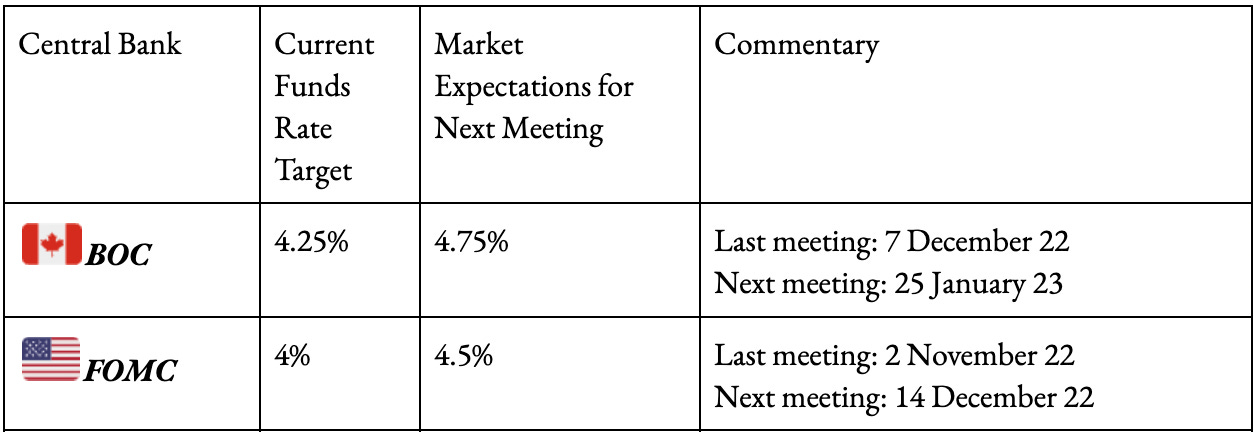

With unemployment higher in Canada, and hence, a more fragile economic situation, the BOC will have a difficult time justifying continued interest rate hikes. In announcing their latest interest rate decision (+0.5% to 4-4.25% funds target rate), they ended by noting that future interest rate decisions would be data driven, signaling that the central bank is close, and flexible in regard to its terminal rate.

Bullish:

-

Oil prices have fallen sharply in recent months. This is a positive news in terms of inflation, and negative news for the strength of the Canadian economy, as Canadian oil exporters are less inclined to expand extraction operations when profit margins are low.

-

Short-term U.S. treasuries are trading at a premium to short-term CAD treasuries, suggesting that investors believe the threat of recession is higher in the U.S. than in Canada. Now that recession concerns have taken to the driver’s seat, demand for the reserve currency should return.

-

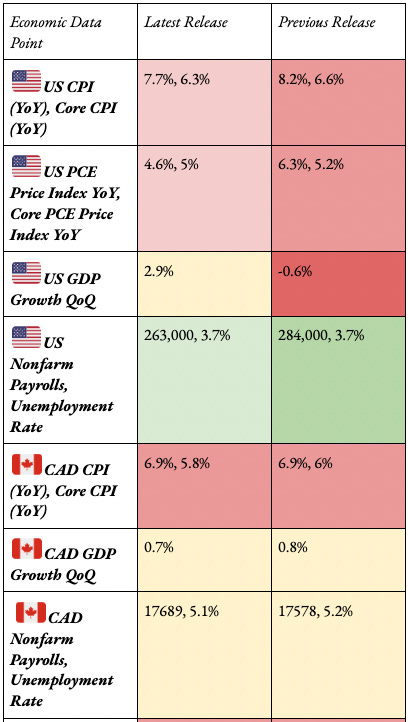

The recent CAD inflation report came in as expected at 6.9% YoY with a core reading of 5.8%. The lack of improvement makes the pair vulnerable to USD strength.

Bearish:

-

Fed rate hikes are likely to ease to 50 bps at the December FOMC meeting, and possibly fall to 25 bps at February and March meetings. The forecast for the Fed’s terminal rate has dropped to 5-5.25%. This range has been more or less confirmed by Fed Chair Powell in his 11/30 speech. Optimism for a “soft” economic landing is waning, but could easily be regained.

-

The price of oil has found a lower bound in the U.S. government announcement that it will refill the SPR if prices fall to $70/barrel. This large influx of demand has created a price floor. The question is, is this price high enough to incentivize production, or will the optimism for the reopening of the global economy return and boost demand naturally?

Overall: Bullish (Daily), Bullish (Intermediate Term). The feeling of optimism for the U.S. economy has dwindled as market participants’ concerns transfer from peak inflation to the ramifications of recession heading into 2023. The Fed’s forward guidance has not shifted since November. The top of the tightening cycle may be Q1 ‘23, but the duration for which rates will need to be held at this level to squash record inflation will only be determined by economic data as it comes. Recent inflation reports (CPI, PPI, and PCE) are showing signs of improvement, but the Fed will not be head faked by one month of positive reporting. The price of oil has fallen significantly in recent months. A looming U.S. recession threatens Canada’s primary exports, which will weaken the Canadian currency. The BOC raised rates by 50 bps at its interest rate meeting. This is in line with what the Federal Reserve will do at the FOMC rate decision meeting next week, and thus should have little effect in the market. Price action suggests weakness in CAD. If upcoming PPI and CPI reports are strong, it could renew the possibility for a “soft” landing in the U.S. if the Fed is able to pivot sooner than projected. While oil sustains its sluggish lows near the SPR price floor, I believe prospects for CAD are weak, and I will be increasing my long position for the pair.

Upcoming events affecting USD/CAD:

-

U.S. PPI (MoM)—12.9

-

U.S. CPI (MoM)—12.13

-

Fed Interest Rate Decision—12.14